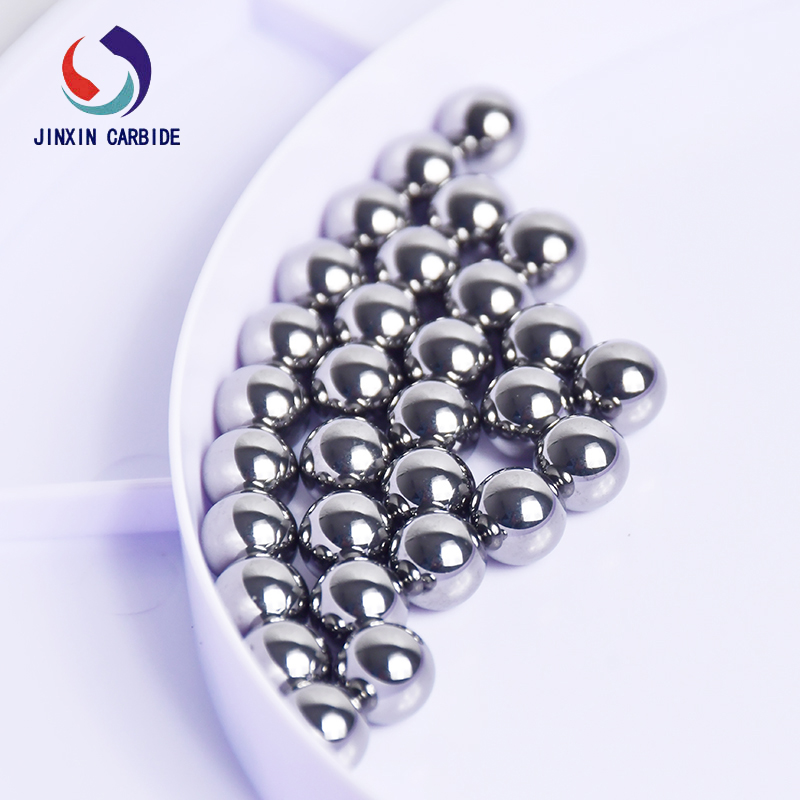

Global Tungsten Prices Surge, Driven by Supply Shortages and Booming Demand for Tungsten Balls

March 18, 2026 — The global tungsten market is experiencing an unprecedented sharp price surge, with international prices of tungsten products, including tungsten balls, continuing to climb steadily amid tight supply and strong demand from multiple high-end industries, according to the latest data released by international non-ferrous metal market research institutions. As a critical component with irreplaceable advantages in defense, aerospace, medical, and photovoltaic industries, tungsten balls, known for their high density, exceptional hardness, and strong corrosion resistance, have become a key driver of the growing demand for tungsten resources, further exacerbating the global supply gap that has been widening since 2024. This price rally has not only affected upstream mining and smelting enterprises but also sent ripples across downstream manufacturing industries worldwide.

On March 18, the European APT (ammonium paratungstate) price, a core indicator reflecting the trend of the global tungsten market, ranged from 2080 to 2270 US dollars per tonne-degree, marking a 2.3% increase from the previous trading day. This price is equivalent to 126,500 to 138,200 RMB per tonne when converted at the current exchange rate, with a cumulative increase of over 130% since the beginning of 2026—an unprecedented growth rate in the past decade. In the U.S. spot market, the price of 99.95% pure tungsten powder at the Port of Baltimore reached 355-360 US dollars per kilogram, a premium of about 185 RMB per kilogram compared to domestic Chinese prices (which stood at around 290-295 US dollars per kilogram). This significant price gap highlights the severity of the global supply shortage and the urgent demand for high-purity tungsten products in overseas markets.

The ongoing price surge is mainly driven by two interrelated factors: tightening global supply and booming demand from key industries, with neither factor showing signs of easing in the short term. On the supply side, global tungsten concentrate production quotas have continued to shrink due to resource protection policies and environmental constraints. The 2026 global tungsten concentrate production quota was reduced by 8% year-on-year to 115,000 tonnes, a cumulative reduction of 14% compared to 2024. As the world’s largest tungsten supplier, accounting for 80% of global tungsten output, China has implemented stricter export controls since early 2025 to protect its scarce strategic mineral resources. Customs data shows that China’s total exports of tungsten smelting products and materials in January-February 2026 dropped by 27.6% year-on-year, with APT exports falling to zero, further limiting the global supply of tungsten raw materials. Additionally, high-grade tungsten ore resources are increasingly scarce globally, with average ore grade declining and mining costs rising, leading many small and medium-sized mines to suspend production.

On the demand side, the rapid popularization of N-type solar cells has driven an explosive surge in demand for tungsten wire, a key raw material for tungsten balls. In 2026, the penetration rate of tungsten wire diamond wires in the global photovoltaic industry exceeded 80%, doubling the tungsten consumption per gigawatt of photovoltaic modules. With the global photovoltaic industry expected to add over 500GW of installed capacity in 2026, the demand for tungsten wire is projected to grow by 85% year-on-year, further straining the supply chain. Meanwhile, the defense and aerospace industries have become major demand drivers amid escalating global geopolitical tensions. Countries around the world are increasing their strategic reserves of tungsten, a critical material for armor-piercing projectiles, aircraft counterweights, and satellite inertial devices. Tungsten balls, in particular, are widely used in precision components like gyroscopic instruments and high-temperature bearings due to their excellent performance.

Industrial Tungsten Carbide Snow Plow Cutting Edge for Heavy Equipment

Industrial Tungsten Carbide Snow Plow Cutting Edge for Heavy EquipmentThe carbide snow cutting edge is designe

Carbide Roller Cemented Carbide Roll Rings/carbide Roller/tungsten

Carbide Roller Cemented Carbide Roll Rings/carbide Roller/tungstenTungsten carbide roller ring is a kind o

Customizable Tungsten Jig Fishing Jig Lure

Customizable Tungsten Jig Fishing Jig Lure97% Tungsten high densityFast production

tungsten carbide forming die

tungsten carbide forming dieCemented Carbide Cold Heading Dies: Prec

Carbide cutting tools grinding carbide/round carbide rods, Cermet metal rods

Carbide cutting tools grinding carbide/round carbide rods, Cermet metal rods1. 100% virgin raw material2. High wear

JX174 Removable Srew-in tire Studs Wheel Snow Carbide Spikes

JX174 Removable Srew-in tire Studs Wheel Snow Carbide SpikesJinxin Studs are widely used in Northern

| WeChat/Phone : | +86 15573301853 |

|---|---|

| Fax : | +86-731-22332243 |

| Email : | jinxin012@ojinxin.com |